Conflating crypto prices and web3 games' future

And more Grinchy reasons why coins don't matter yet

Why crypto prices don’t matter for gaming

Over the past couple weeks, if you live in our little web3 bubble, you’ve probably noticed that crypto prices are rebounding. All over the social medias, people even in blockchain gaming have been hosting Spaces and posting, “We’re back!” as if the price of Bitcoin is a leading indicator of the success of the future of gaming. Spoiler, it’s not.

For those who have braved the depths of the crypto winter—from which these price movements indicate we could be emerging—any glimmer of macro hope is exciting. And if you run the kind of speculative PFP collection or game, it’s even more exciting since now all your holders are that much richer and you didn’t have to do a damn thing. Go you. It also, abstractly, could mean that capital is unlocked for new investments into cash-starved studios or that there’s a resurgence of interest from enterprise companies who are willing to tango with that new-fangled blockchain thing.

Except no. What everyone learned from the last bull market of 2021 was that a surging CoinGecko doesn’t overcome a complete lack of content, delighting experiences, or seamless onboarding. The bull market didn’t onboard “the next billion people.” It didn’t debut the first at-scale game. Instead, it turned crypto into a household name—and we all know how that went.

Because of this association with get-rich-quick NFT projects and token launches, the movement of crypto prices has been conflated with the value of the blockchain as a technology and, in gaming, the benefits of web3-based titles. This is misguided. As I’ve expounded on a lot in these pages, web3 is a tool for developers and players. That’s it. What you do with it, like what you do with an AWS or Google Cloud server, is entirely up to the design of the experience and what will resonate with players and users. Now, to be fair, it’s really the directionality of the association between crypto prices and web3 gaming and consumer apps that is inaccurate; i.e. the price of Eth shouldn’t mean web3 gaming will flourish. In theory the value of cryptocurrencies should be dictated by demand, and that demand could be generated by more activity and more consumer need for crypto currencies. Economics!

Currently, crypto prices have no relationship with demand from in-content activity. The crypto rally of 2021 wasn’t from incredible, sustainable content (though to be clear, it’s coming—good game development takes time!). Token prices were at the whim of investors and traders, who in their part were speculating on the frenzy around PFP collections and half-baked brand campaigns in web3. The whole value system was built on twigs propped up by jpegs and Fortune 100 activations. Just as today the rally isn’t because GTA VI is going to be a web3-based game, it’s because there might be a Bitcoin ETF, and all crypto tides rise by the same moon.

Indeed, the volatility in crypto prices was one of the things that turned many gamers (and developers) away in the first place. If you didn’t buy Bitcoin when it was $1.00, you didn’t have funny money to play with and a game token could be $40 one day and $100 the next. Not great. The greed inherent in much of the movement of cryptocurrencies also didn’t help the image amongst gamers or regular consumers that the whole thing was a cash-grab. And beyond that, those that felt they had missed out on the opportunity to get rich turned that FOMO into loathing.

Far from being a result of content and mass adoption, crypto prices have perhaps done more harm than good to the industry.

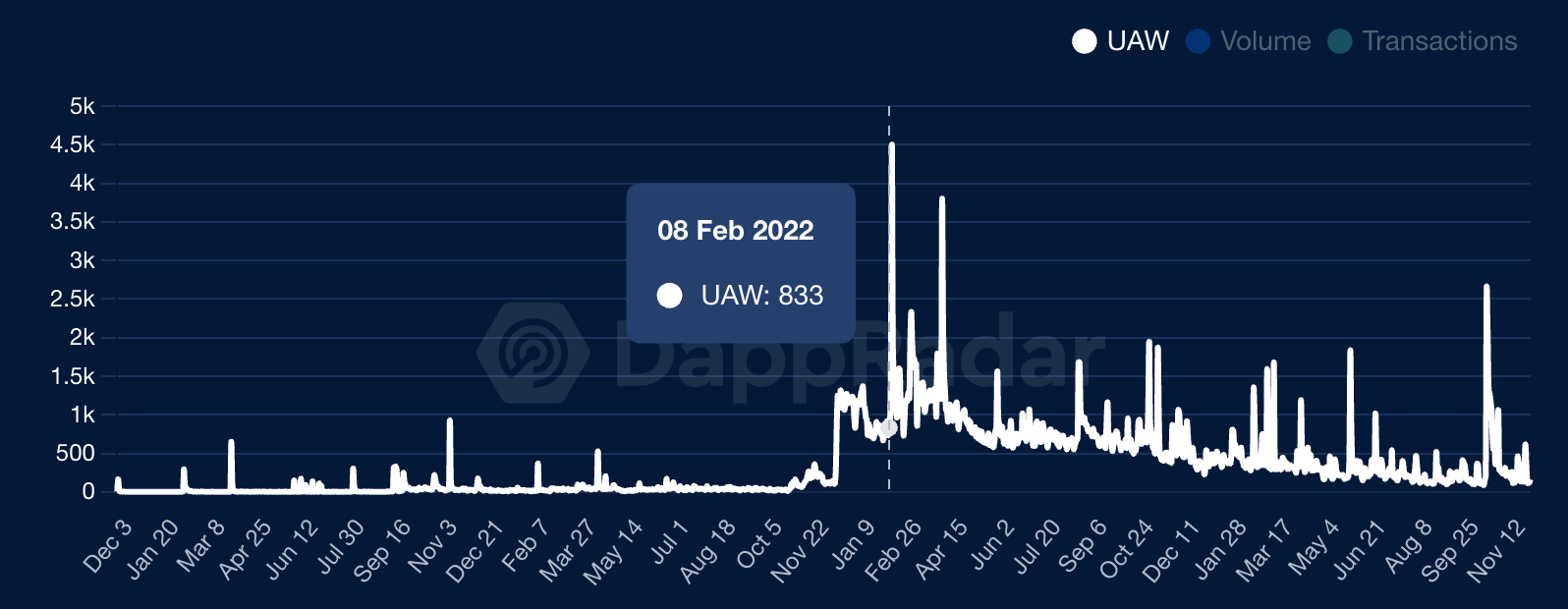

Token prices, especially so-called “utility” tokens that many companies launched during the hype cycle, were equally divorced from any in-game or player activity and instead followed exactly the same (if not worse) trajectory as the major currencies did. As we can see below for SAND (the token launched by The Sandbox), the coin’s price moved identically to Eth (in red) and Bitcoin (in orange) and actually failed to recover to the same degree as the latter two did during that brief bump around July 2022.

Moreover, SAND’s peak price happened a full three months (in November 2021) before the game’s peak unique active wallets (UAW) in February 2022, when the price was in complete free-fall. To put it another way: at the time when the game supposedly had its highest performance, the price of SAND in no way reflected that engagement. That’s not a ringing endorsement to developers who would hope that increased engagement with their game could result in a better coin value and therefore a richer developer and ecosystem.

Could this just be a matter of scale? Maybe. A whole 4,000 wallets (not humans, just wallets; not players, just wallets) is not going to get any economy that’s actually engineered only for a handful of market-making degens frothing with value. And of course, until recently, web3 has had a bit of a problem with scale: the entire ecosystem being little more than a rounding error to even the most modest mobile game. Ongoing regulatory issues have also made it challenging for companies to inject coins into games with any significant level of usage. Less utility, more speculative side show.

I’m not trying to be a party pooper. But I do encourage the industry to spend less time ballyhooing the supposed return of the bull market at a cost of doubling down on a focus on content, seamless onboarding, and proving that the masses should be here because there’s something for them. The next billion users do not care about the price of Eth, of SAND, or of any other coin. They care about what amazing experiences are here for them, and an industry that touts mercurial currency prices over the fundamental value of the content and performance of experiences is not far removed from investors who congratulate and reward the stock price of game developers for canceling games and announcing layoffs. And we all know how that makes us feel.