Last week, the NFT marketplace Recur announced it was closing. This was part of a rough week for third party/licensed NFT marketplaces (Yuga Labs announced it was bailing from OpenSea amidst their unwillingness to enforce royalties as a result of competition from speculator marketplace, Blur).

Recur had raised $50M with a peak-hype valuation of $333M. Its death is one of the biggest non-FTX-type failings in web3 so far—a good and legitimate company—and it’s reflective of a model that was structured against its long term future.

Here’s what happened, why it is vital for brands to think differently, and what this means for third party marketplaces going forward.

Recur didn’t stand a chance

Recur was a third party NFT marketplace, but one that did a lot of its own drops via licensed content collections with major IP. It was a poster child for the 2021/22 NFT craze’s intersection of web3 and the early experiments of traditional brands and media.

It was a scenario where:

Recur spent LOTS of money acquiring IP licenses, leaning into nostalgic Nickelodeon content

Recur owned ALL problems in the stack:

a) it was the tech platform

b) it was the liquidity provider

c) it was the content studio

d) it was burdened with all user acquisition

BUTRecur had no power. When speculation died, which it always would, the platform had no ability to influence the utility and game plans of the licensors. It was a lunchbox maker who slapped on familiar stickers, but had no ability to determine the destinies of what these IP holders would (or should) intend for the future of these items. Do they unlock merch or become game pieces? For Paramount’s Nickelodeon IP, in this example, it was just a minimum guarantee and royalties, not a comprehensive future. So for Recur, there was nothing to leverage beyond the secondary trades (which, like most NFTs from web2 brands, didn’t benefit from ongoing degen flipping), and start all over to spend more for the next drop, and the next drop, and the next drop.

I've written about the pitfalls of licensed IP in web3 gaming, which at least has the benefit of a utility end-game (the game itself). PFPs like Rugrats’ have none of that, unless built with that plan from the ground up. Recur was at the mercy of a broad strategy that was absolutely necessary for the future covet-ability of the items it sold, but one which they had no control over.

Web3 is too new for upstart platforms like Recur’s to successfully leverage existing IP but be kept at arm’s length by the IP holder. Unlike a merchandizer who will license Tommy Pickles for a t-shirt and has a vast network of distributors and retailers who already have the traffic of relevant fandom regardless of advertising from Nickelodeon itself, NFT platforms have little to no access to the key audience, i.e. fans that want to buy the items for love of the IP and because of access/benefits it gets them.

In fact, the @Nickelodeon Twitter account never once messaged the relationship with Recur, the NFT launches, or digital collectibles. Nor did the @ParamountCo account.

We’re at the point where an IP that doesn’t have complete ownership and responsibility for its web3 existence is akin to Pixar debuting Toy Story 4 and Disney never hearing about it.

What this means for brands

Existing IP holders now have proof in the pudding that a traditional licensing model in web3 through pure collectibles or digital merchandise has no legs if it’s not coming natively from the company itself (Nike, LVMH, Reddit, Starbucks are all examples of more sophisticated and long-term plays). Taking things in-house has not only the potential to integrate into the core business and flywheel of the company holistically, but it also de-risks some of the challenges unique to web3 and NFTs.

While Recur had no influence over Paramount, Paramount likewise had no stake in Recur and its future. If the Tommy Pickles t-shirt maker above goes out of business, no one cares. The items are sold, it’s over and done with. But NFTs—regardless of who makes them—are seen but consumers as having a deep connection to the IP holder, and many (even if misguidedly) see them as investments into that IP that constitutes a forever relationship.

Now, Paramount has thousands of angry PFP holders. Unlike with bad merch that can be pulled from shelves and the manufacturer thrown under the bus, these items live publicly, digitally, forever. Recur is no longer, but the sentiment around those items—ever-present in consumers’ wallets and accounts—will be a constant reminder of a strategy that dead-ended.

What this means for marketplaces

Which is why the future of this space is in-house and corporate. IP holders can't simply license under an old model. These are the loyalty passes that fans will take into dozens of experiences, and it's in the best interest of the IP to bring as much of that under one strategically-unified roof as possible.

That means white-labeled wallets and onboarding experiences, white-labeled marketplaces. But, most importantly, white-labeled strategies that don't jump on the PFP hype bandwagon of 2021 but actually integrate into the longer term plans of how companies will interact with their fans through the blockchain.

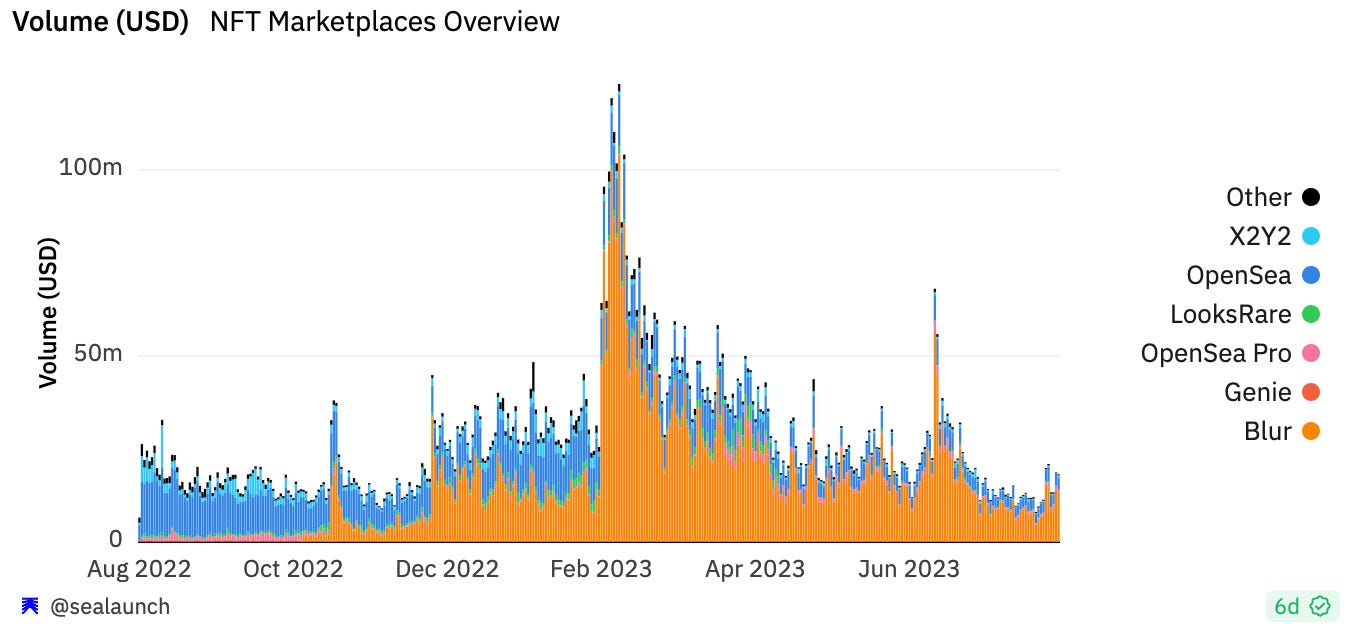

Adding fuel to this shift’s fire was Yuga Labs’ decision—also announced last week— to pull away from OpenSea because of the platform’s lack of royalty enforcements. The royalty debate heated up over the last year or so, as hardened NFT flippers aimed to eek out every ounce of alpha possible, and 2-7% of royalties paid to the original creators was just out of the question (and, hilariously, beyond hypocritical to the OG ethos of web3…).

OpenSea’s royalties plan came after eight months of tough marketshare loss to Blur, the NFT marketplace built for the professional speculator and trader class. Hoping to regain the degen traffic, OpenSea has opted for a plan that, unfortunately, appeals more to a few thousand traders than the needs of future corporate entrants in web3.

Ultimately, all the marketplaces listed above face a challenging future with their current models as the NFT space continues to shift toward free or low-cost gaming and loyalty based items, ones with more utility than secondary market value, and ones whose existences will be driven by native, in-house branded ecosystems and markets that live where users expect them: in the game, in the mobile app, in their existing account.

Behind Yuga’s announcement was a veiled message that reflected and accelerated an inevitable need: having experiences and UX that they own and control, meant for meaningful usage more than flipping. This is a big move and a staggering line in the sand for a company that owns the most recognizably speculative assets in NFT-land. In choosing to not be held hostage by a handful of traders, Yuga is further declaring that its future relies on owned experiences and in-game utility, not on third party ecosystems.

Recur is just the first in an upcoming mass extinction of companies that were stuck in a position that put them at odds with the beneficiaries of a future that looks and feels more like ones consumers are used to, but merely driven by the blockchain in the background.